Year of the yuan: China's explosive currency goes global

Published 1 May, 2013 07:51 | Updated 1 May, 2013 08:21

The ‘people’s currency’ of China is redefining the global economic monetary system. The closed-capital pariah is blossoming into a reserve standard and is hedging appeal against the indebted dollar and the untested euro, piquing foreign interest.

Degenerating credit quality across the board has prompted asset

managers to shy away from the dollar, euro, Japanese yen, British

pound, and Swiss franc. And some are turning to the yuan, a

currency that 10 years ago was completely off limits to foreign

investors.

An HSBC forecast projected that by 2015, the yuan will become one of the three most used currencies in global trade, in league with the dollar and euro. The report, issued in April, also foresees a third of China’s cross-border transactions being carried out in yuan.

China has been making a concerted effort to establish itself as an international currency reserve. China already has agreements with Russia, Vietnam, Thailand, and Japan allowing trade to be settled in yuan instead of dollars

Circulation of Global Payments - January 2013 SWIFT DATA

1. Euro 40.17%2. U.S. Dollar 33.48%

3. British Pound 8.55%

4. Japanese Yen 2.56%

5. Australian Dollar 1.85%

6. Swiss Franc 1.83%

7. Canadian Dollar 1.80%

8. Singapore Dollar 1.05%

9. Hong Kong Dollar 1.02%

10.Thailand Baht 0.97%

11.Swedish Krona 0.96%

12.Norwegian Krone 0.80%

13.Chinese Yuan 0.63%

14.Danish Krone 0.58%

15.Russian Ruble 0.56%

As China launches its global currency, European financial centers are hoping to become Europe’s yuan hub. London, Paris, and Zurich have all made very vocal bids for this title. According to Bloomberg, the Bank of England has an inside track to be the first Group of Seven nation to sign a currency-swap with the People's Bank of China. The deal may grant the UK central bank as much as 400 billion yuan ($64 billion) in reserves.

Many national banks are switching over to the yuan to diversify their reserve currencies, Australia the most recent to join ranks with the world’s second largest economy.

The Reserve Bank of Australia announced in April it will transfer 5 percent of its foreign currency reserves ($2.1 billion) into Chinese bonds, deepening ties with its Pacific neighbor and biggest trade partner, and reflecting a global shift to the yuan.

The move is an “important milestone in deepening our financial and economic linkages with China,” Australia’s Treasurer Wayne Swan said in an emailed statement to Bloomberg.

China and Australia are major trading partners, so an investment

in Chinese currency reserves will benefit transactions between the

two countries. Now, they can conduct business transactions directly

from yuan to Australian dollar, cutting out the middle man, the US

dollar or euro.

The Chinese yuan is the 13th most-used currency in the world for international payments, according to a February 2013 report by the Society for Worldwide Interbank Financial Telecommunication (SWIFT). It jumped 6 places from the previous year.

SWIFT reported that the value of payments in yuan soared $171

year-on-year in January, or 24 percent. The yuan has

surpassed the Russian rouble and the Danish krona in international

transactions. Close behind are the South African rand and the New

Zealand dollar. The euro is the most used currency, followed

by the US dollar, and then the British pound.

The debut

The yuan has been dubbed a ‘hermit currency’, isolating itself

from foreign investment and setting its own rules, but is now

slowly entering world currency markets.

“The hermit is ready to come out of its shell and the sooner the

better for China to play a major role in the global economy,”

said Patrick Young of DV Advisors.

Cross-border yuan payments through Singapore rose 30 percent

month-on-month in January 2013. Payments through London grew at an

even faster pace, at 40 percent, according to the HSBC report.

The top-five currencies for international payments in January 2013 were the euro (40.17 percent), the US dollar (33.48 percent), the British pound (8.55 percent), the Japanese yen (2.56 percent), and the Australian dollar (1.85 percent).

“The Yuan will take its place as a leading global currency, it is not likely to challenge the dollar's hegemony for some time, ” Patrick Young said.

In 2012 there was a 900 billion yuan ($145 billion) increase in

trade payments, according to The Economist. Only three years

ago there were almost zero transaction payments settled in

yuan.

“The world's reserve currencies are distributing away from

dollar centrality to a broader spread of currencies. To that end

the Yuan and indeed the rouble are all likely to take a greater

share of global reserves as indeed the economic power of the east

expands,” Young added.

Recent economic problems linked to the euro and the dollar have

set a trend for currency reserve diversification as an alternative,

Yaroslav Lissovolik, chief economist at Deutsche Bank in Moscow

told RT.

“It is definitely a trend and this trend will continue. There is a

global demand for more reserve currencies. The world economy wants

to diversify the set of reserve currencies as a way from the

volatility and the problems associated with the current reserve

currencies, because both the US and Europe are plagued by economic

problems. This is natural and clear that the global economy should

use more foundations, more columns on which to stand and build a

stronger foundation of a more complex global economy,” said

Lissovolik.

The numbers are on the rise, but they still pale in comparison to

the dollar. The yuan only comprised a 0.63 percent market

share of the global currency market as of January 2013. Its ranking

is still a minute fraction of China’s export market, the world’s

second-largest, after the EU.

The dollar, the current market and commodity standard, totals $11

million in currency reserves.

‘Dim sum bonds’

Another pin in the narrative of the yuan is Hong Kong and ‘dim sum bonds’.

The yuan hasn’t been officially available for foreign trade, but ‘dim sum bonds’, a bond dominated in Chinese yuan assets and issued in Hong Kong, has allowed foreigners a loophole to invest in domestic Chinese debt.

China has set up special administrative regions in Guandong province, Hong Kong and Macau, which operate with their own currencies, but are still closely linked to the Chinese economy.

Hong Kong has long served as a roundabout way to get exposure to China’s closed capital market, but still only equal about 1% of those in mainland China. The offshore status allows foreigners to circumvent the tight currency controls through the financial hub.

The more offshore (or ‘onshore’, in the case of Hong Kong) deposits that are out of the control of the PBoC, the less effective the capital controls are.

History of currency manipulation

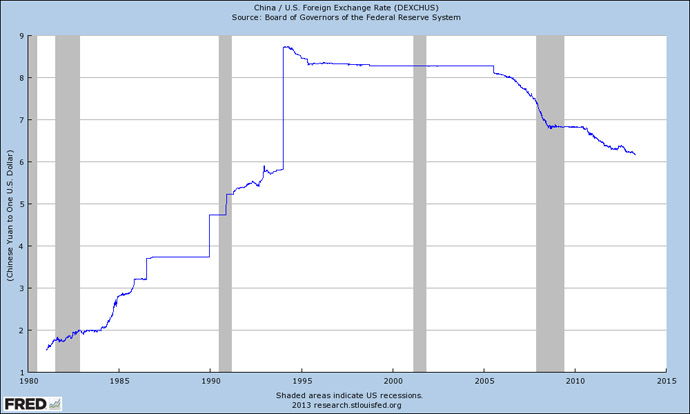

The yuan hit a 19 year high on April 26 at 6.1616 against the dollar after the PBoC loosened controls on the reference rate to increase investment, as well as an effort towards making the yuan a ‘floating’ currency by 2015.

In 2012, the yuan advanced 1 percent against the dollar, but in 2013, it could appreciate between 2.1 percent to 6.1 percent, according to a Bloomberg survey.

China insulates the yuan under strict government controls but has recently taken steps to trim the nation’s reliance on the dollar by establishing demand for their own currency.

China severed its currency peg to the dollar in July 2005 after 10 years of a stable, almost unchanging exchange rate.

Before 2009, the central government had prohibited export of the currency and its use as tender in international transactions.

By keeping the floodgates of market volatility closed for more than a decade, the value of the yuan has been set at an artificially low level, which in part facilitated China’s 30 year export boom. China enabled its currency to strengthen 21 percent between July 2005 and July 2008, including an inaugural single-day gain of 2 percent.

With almost no international capital flow, the fixed currency safeguarded China from the Asian financial crisis of 1997 and the US banking crisis of 2008 and subsequent world recession.

Appreciation efforts were cut off to brave the global recession and climbed 10 percent against the dollar since the state deregulated controls on June 19, 2010.

The consensus among politicians and economists alike is that the yuan is expected to ‘float’ in 5 years.

Before the yuan can ‘float’, be dictated by markets and not government manipulation, China will have to restructure its interest rate system, which, currently set by the state, has little maneuverability and range.

If China accelerates the process, implications are bullish. A higher interest rate will slow investment expansion and growth, which will kick back GDP. If the yuan becomes too expensive too quickly, it will hinder export demand, a lifeline to China’s economy which has kept it relatively unscathed from the worldwide recession.

If the yuan rises too quickly, it will also inflate prices, which could force toy, textile, and electronic factories to move inland in search of cheaper labor.

China’s growth has slowed to 7.7 percent in the first quarter, missing the 7.9 percent benchmark of the previous quarter. China must find closely monitor its growth slump in tandem with currency valuation. Because of its export-driven economy, relinquishing full control of the currency in the short-term is highly unlikely.