Has Europe really recovered from its 2008 financial meltdown?

The mainstream media, and the economic pundits it favors, are rejoicing in the idea that Europe is “back in business,” following a fallow decade. A quick glance at Spain’s numbers suggests this hope may be forlorn.

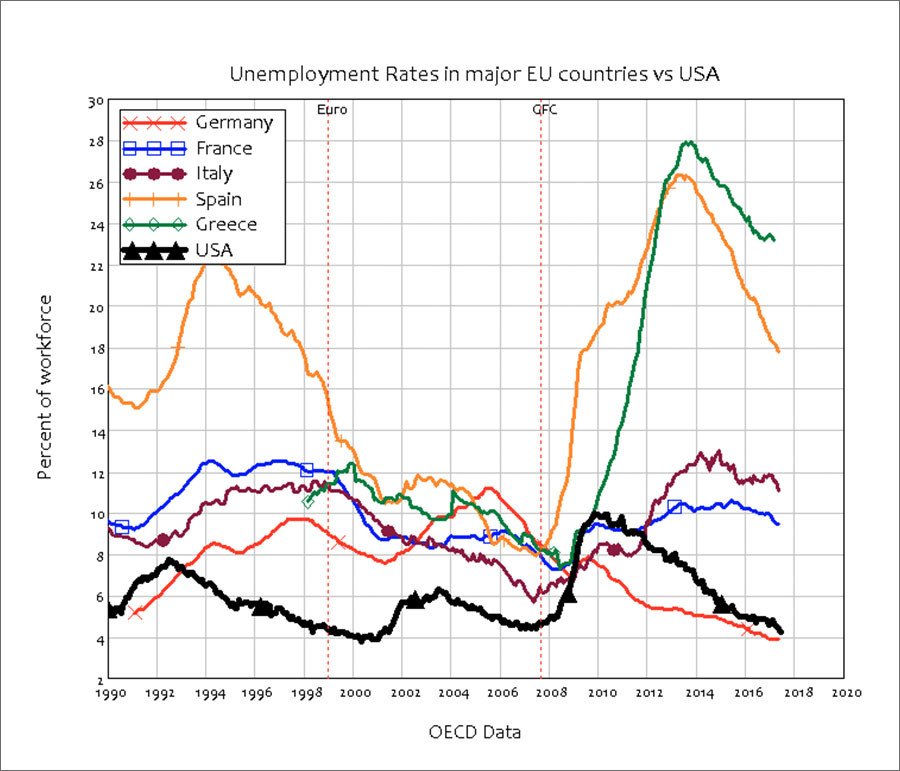

With the exception of Germany, unemployment in major European Union countries has not returned to pre-crisis levels. Spain and Greece still have Depression levels of unemployment. France and Italy still have very high unemployment, with Italy having only recently fallen below the worst levels it experienced between 1990 and the introduction of the euro.

But unemployment is nonetheless falling across most of the EU, and 10 long years after the financial crisis began in 2008, people are finally asking whether the worst is over.

Nobel Prize winner Paul Krugman certainly thinks so, speaking of the “significant recovery finally taking place in Europe” (“Notes on European Recovery (Wonkish)” New York Times, February 11, 2018), he attributes the recovery to two factors: the European Central Bank’s promise to do “whatever it takes” to end the crisis, which “almost instantly ended the panic in southern European bond markets,” and “internal devaluation” as the huge squeeze on living standards drove down European wage costs relative to the rest of the world. This has led to “a big export boom, especially in autos.” Consequently, he declares, “Europe is back as a functioning economic system.”

But is it? And was the ECB’s program of quantitative easing (where it guaranteed to buy bonds where the market might not, and pumped trillions of euro into financial markets) and internal devaluation the total solution?

Free money

There’s no doubt that Europe is recovering, and those factors have been part of it. But so is another element which economists, especially Krugman himself, continue to ignore: credit. Not only Europe’s crisis, but America’s and the UK’s as well in 2008, was due to a collapse in credit-based demand. In fact, Europe is back largely because credit is back: European (and American and British) consumers and firms are borrowing once again and unleashing that borrowed money into their economies, boosting demand and lowering unemployment.

This means the recovery can continue only so long as households and firms can keep getting into debt. Yet, given private debt levels are still high when compared to GDP, it won’t be long before the national credit cards are maxed out again. Then the borrowing will stop, and the recovery will run out of steam.

So why aren’t economists warning of this dark lining in the silver cloud of economic recovery? It’s because they don’t think that credit matters, and they ignore it when making forecasts about where the economy is likely to go. Their logic is that credit simply transfers spending power from one person to another, so changes in the level of private debt only affect the economy if the borrower has substantially different spending patterns to the lender. To use Krugman’s own language here, rising private debt will only affect demand if the borrowers are “impatient people” who spend a lot, while the lenders are “patient people” who spend very little.

This implies that large changes in private debt should have only small effects on the macroeconomy.

I could get all theoretical here and prove why this belief is false, but it’s rather easy to show what the biologist Thomas Huxley once described as “no sadder sight in the world,” which is “to see a beautiful theory killed by a brutal fact.”

Reality bites

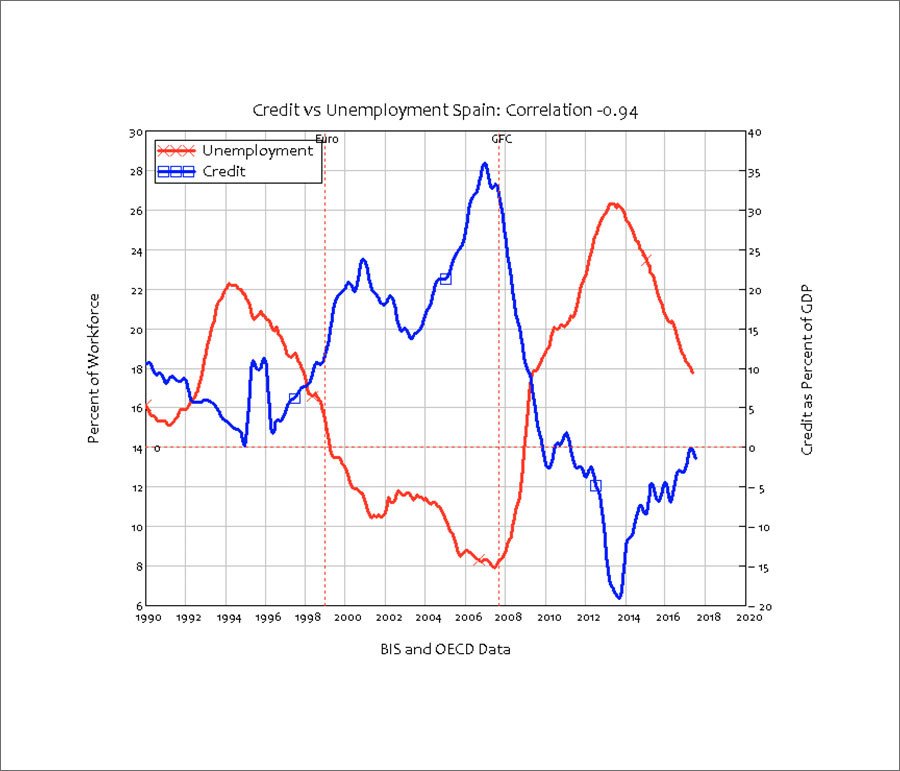

If the theory that credit doesn’t matter were true, then credit and unemployment would be unrelated to each other. But they are! Here’s a killing of this beautiful theory by a brutal fact that’s worthy of a Game of Thrones beheading: Ladies and gentlemen, I give you the relationship between credit (the annual change in private debt, measured as a percentage of GDP) and unemployment in Spain, between 1990 and July 2017 (the latest quarter for which there is data on debt from the Bank of International Settlements).

So there’s no relationship? In fact, it’s an almost perfect negative relationship: credit goes up, and unemployment goes down; credit goes down, unemployment goes up. Spain’s great boom began when credit rose from trivial levels – just over two percent of GDP in 1996, when unemployment was 20 percent of the workforce – to over 35 percent of GDP when unemployment fell to historically low levels (for Spain) of eight percent.

Then boom turned into bust, as credit fell from 36 percent to almost minus 20 percent of GDP in 2013. Unemployment exploded to 26 percent of the workforce, the worst in Spain’s post-WWII history. Then unemployment started to fall again as credit rose – from minus 20 percent of GDP to zero. So, credit isn’t adding to demand in Spain right now (and it’s turned slightly negative again in the latest data, for July 2017), but it’s no longer subtracting from demand either.

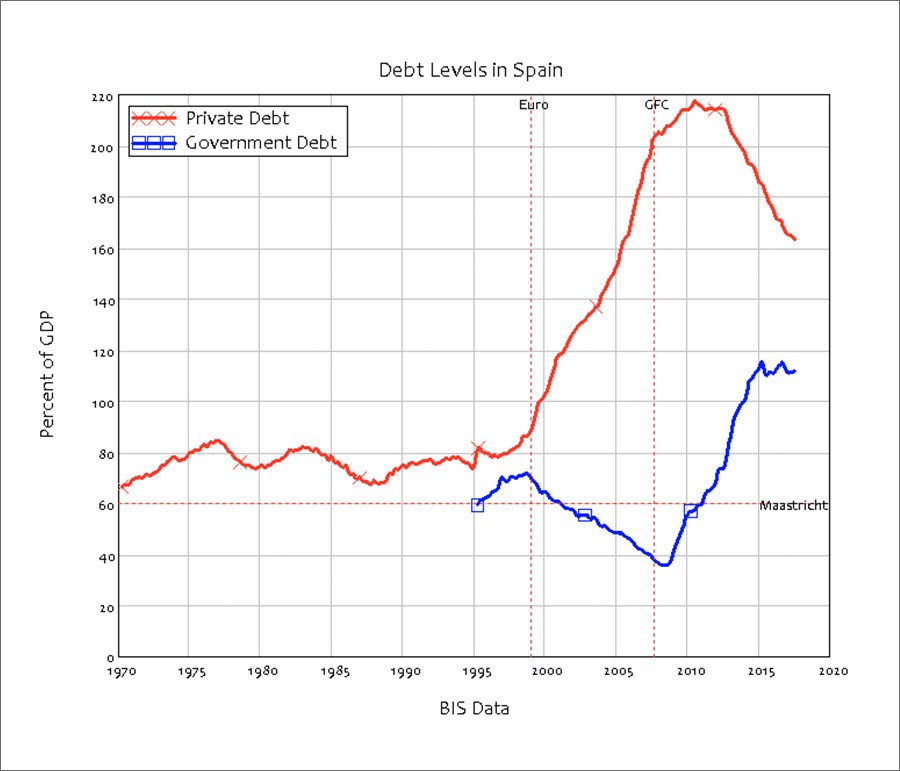

Will credit continue to grow, and it help drive unemployment down below its current level of 16 percent of Spain’s workforce? It can for a while, but there are two things that will stop credit growing: the level of private debt today; and the EU’s obsession about reducing Spain’s government debt levels from 100 percent of GDP, as they are now, to below the Maastricht Treaty ceiling level of 60 percent of GDP.

History repeats

Spain’s private debt levels have fallen substantially since the worst of the crisis – from 220 percent to 160 percent of GDP – but they are still way above historically sustainable levels for Spain of about 80 percent of GDP. As interest rates rise and the European Commission puts a squeeze on government spending in Spain, households and firms will find debt servicing difficult and shall go back to reducing their debt levels, rather than increasing them. That will end the recovery and push unemployment back up again.

Why am I so pessimistic? Because I’ve seen this movie before, and I know the ending. It was called the Roosevelt Recession in the 1930s, when President Roosevelt accepted the advice of his economic advisors that the worst of the Depression was over – with unemployment having fallen from 26 percent in 1933 to 11 percent in 1937 – and it was time to rein in government spending after the New Deal.

Government spending fell, interest rates rose, and the private sector went back to reducing its debt in response. Unemployment exploded again to 20 percent of the workforce by mid-1938, and only gearing up for WWII drove it back down again.

That lesson was not learnt, because of all intellectual traditions, mainstream economists are most subject to Santayana’s aphorism that those who do not study history are doomed to repeat it. And as a rebel economist who does study history, I am doomed to watch them repeat it, at the eventual expense of this nascent recovery in Europe.

The statements, views and opinions expressed in this column are solely those of the author and do not necessarily represent those of RT.