Can Tesla live up to its $400 billion valuation?

Published 5 Sep, 2020 12:52

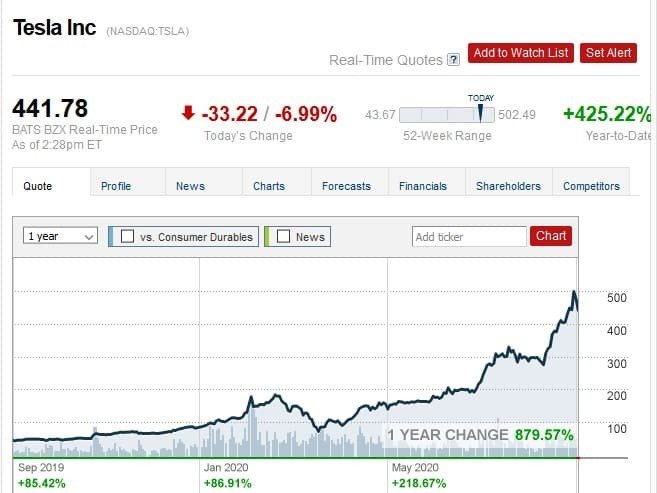

Tesla stocks have rallied almost 1000% over the last 12 months, and while the stock is finally cooling off, the question remains whether the company can really live up to its valuation.

By any yardstick, the world's most popular electric vehicle manufacturer, Tesla Inc. (NASDAQ:TSLA), is enjoying a banner year. Tesla's parabolic rally has been nothing short of extraordinary, with the shares at one time exceeding a 1,000% gain over the past 12 months and nearly 500% in the year-to-date. At one point, Tesla was even more overbought than Bitcoin during the mad December 2017 rally after TSLA's 14-day relative strength index (RSI) metric touched 92.5 compared to Bitcoin's all-time high of <91.

The mad rally has forced even permabears such as Morgan Stanley's Adam Jonas and Bank of America's John Murphy to capitulate on their Sell ratings as everything seems to go Tesla's way.

Also on rt.com Chinese electric car maker Nio ready to challenge Tesla in major global marketsThat said, TSLA finally appears to be cooling off, shedding 11% just two days after the company announced a $5B capital raise by selling shares in the secondary market, a move that represents a mere ~1% share dilution.

Still, TSLA's current RSI reading of 72.1 suggests the shares have been burning rubber and have possibly entered bubble territory. Further, TSLA still boasts a market cap of $413B, easily the highest by any automaker.

Is Tesla's steep valuation justified, or has it become just another cult stock and a disaster waiting to happen?

What is fueling the insane rally?

Defying bearish expectation

There is no way to sugarcoat this: Tesla's valuation looks absurd, whichever way you dice it.

Tesla's market cap is now bigger than Toyota Motors' (NYSE:TM) $215B, and several times bigger than the combined valuation of the US 'Big Three': General Motors (NYSE: GM), Ford Motor Company (NYSE: F) and Fiat Chrysler Automobiles US (NYSE: FCAU) with market caps of $44.3B, $27.1B and $17.13B, respectively.

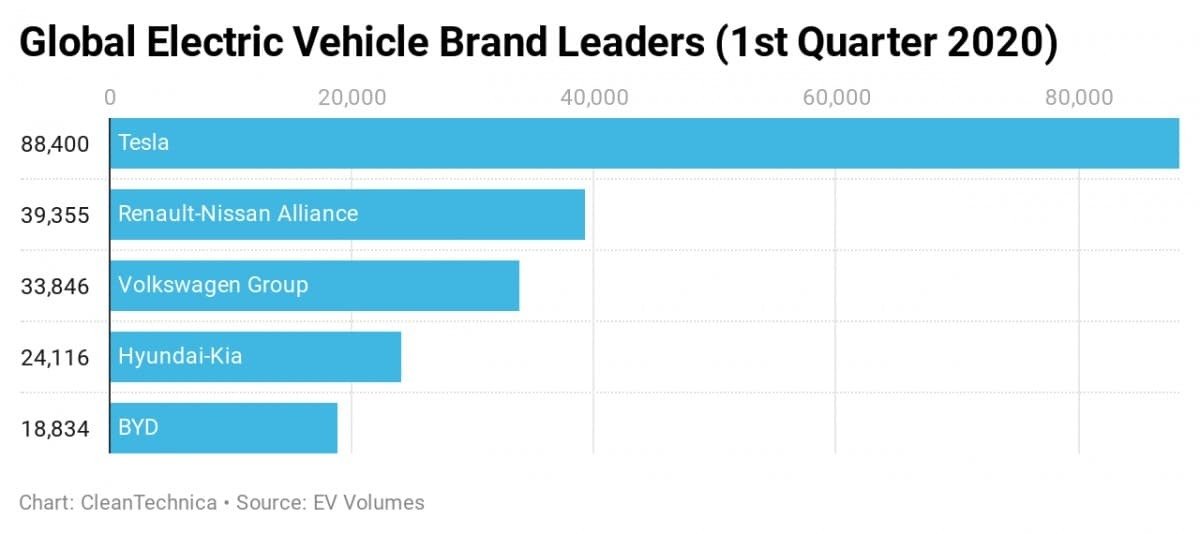

During the last quarter, the Palo Alto, California-based EV manufacturer delivered 90,650 vehicles, easily smashing the Wall Street consensus of 83,000 units. The highest forecast was for ~86,000 units.

A big reason for Tesla's impressive numbers is its new Gigafactory in Shanghai, which remains on course to exceed production of 100K units during its first year in operation. That will help Tesla achieve its goal to sell 500K units in the current fiscal year.

It is noteworthy that all three ICE manufacturers recorded double-digit sales declines compared to a three percent Y/Y fall by Tesla. That is impressive because Tesla has been defying bearish expectations that low gas prices were going to slow down the electrification drive and discourage prospective buyers from shifting to EVs.

Still, Tesla sales are a mere fraction of the 1.29M units sold by the Big 3 during the quarter.

Tesla's current market cap implies that the company will be able to sell more than 6M units, or one-in-four of global EV sales, by 2030, marking a 12-fold increase in production output in just a decade. That won't be an easy feat to pull off considering that Tesla's global EV market share currently stands at 19%, and also when you take into account that Tesla brands will be competing against nearly 500 other brands, or 10X the current number of EV brands globally according to BNEF estimates.

Other reasons have been advanced to explain Tesla's crazy rally.

One is that Tesla is emerging as the energy king.

Wall Street has been saying that Tesla's next challenge will be to convince its EV customers that charging their vehicles using coal-based electricity is not very green and urge them to generate and store their own solar power. Piper Sandler's Alexander Potter and Winnie Dong say that their experiment to install a solar system to charge a Model X has already yielded "illuminating" results and "shows significant promise" for Tesla's future in the energy-generation industry.

Tesla's acquisition of SolarCity for close to $5bn in 2016 might turn out to be one of its best decisions in hindsight, given how well renewable energy stocks have been doing and the ESG megatrend. Further, Tesla's extreme vertical integration is beginning to yield dividends.

However, solar and battery storage remains an auxiliary business for Tesla, bringing in just ~5% of revenues.

Yet another reason is Robinhood, the zero-commission app that has brought hundreds of thousands of younger investors into the market. Tesla has consistently ranked among the most popular stocks on Robinhood, raising concerns that a group of naive investors is driving the rally. Indeed, Tesla shares have been rallying even harder after the company announced a 5-for-1 stock split., climbing 49% over the past 30 days. The same stock split mania has overtaken Apple Inc. (NASDAQ:AAPL) with the shares up 20% in the space of a month after the company announced a 4-for-1 stock split.

Tesla's latest 13G filing has revealed that individual shareholders and insiders own about 20% of the company, certainly big enough to cause some havoc.

Cracking the Tesla code

Whereas all these catalysts could be working in tandem to propel Tesla to its stratospheric valuation, perhaps nothing explains the torrid run better than Bank of America's John Murphy, who appears to have cracked the Tesla code:

"Building capacity in the automotive industry is expensive and often generates low returns. Even if there is a future software/service/ride-hail play for TSLA (and we have our doubts), the vehicles/platform still need to be manufactured. It is important to recognize that the higher the upward spiral of TSLA's stock goes, the cheaper capital becomes to fund growth, which is then rewarded by investors with a higher stock price. The inverse of this dynamic is also true, and it is this self-fulfilling framework that appears to explain the extreme moves in TSLA stock to the upside and downside."

Also on rt.com Tesla's newest rival is taking the stock market by stormMurphy says that whereas Tesla may or may not become dominant in the long-term, investors are more focused on the fact that it can continue funding outsized growth with almost no-cost capital driving capacity expansion.

Long-time Tesla investor, Baillie Gifford, has pretty much a expressed a similar sentiment:

"...We remain very optimistic about the future of the company. Tesla no longer faces any difficulty in raising capital at scale from outside sources but should there be serious setbacks in the share price we would welcome the opportunity to once again increase our shareholding."

Also on rt.com Tesla becomes 10th largest US company by market value after stock breaks all-time highGiven the amount of goodwill Tesla is enjoying, it might even decide to buy the ICE heavyweights themselves or even highly profitable companies in other sectors, thus boosting its profitability overnight.

However, that does not mean that Tesla does not carry significant downside risk. As one analyst has warned, TSLA stock could very well take Amazon Inc.'s (NASDAQ:AMZN) early trajectory that saw the e-commerce giant crash to earth during the Dotcom burst before later becoming the most dominant player in the sector.

This article was originally published on Oilprice.com