Bear run sends oil down for 10th straight session

Published 5 Feb, 2020 09:29

A bear stampede has taken hold of oil markets as the coronavirus continues to spread fear, uncertainty and doubt.

Oil futures slid for a 10th straight session Monday as casualties hit 426 and the number of infections surpassed 20,000.

And now big money managers have joined the stampede as new data reveals the virus is creating severe demand shocks that could further depress prices. Reuters has reported that fund managers and hedge funds were heavy sellers of crude oil and various refined products last week as the worsening outbreak heightened fears of a demand meltdown in China, the world’s leading importer of crude.

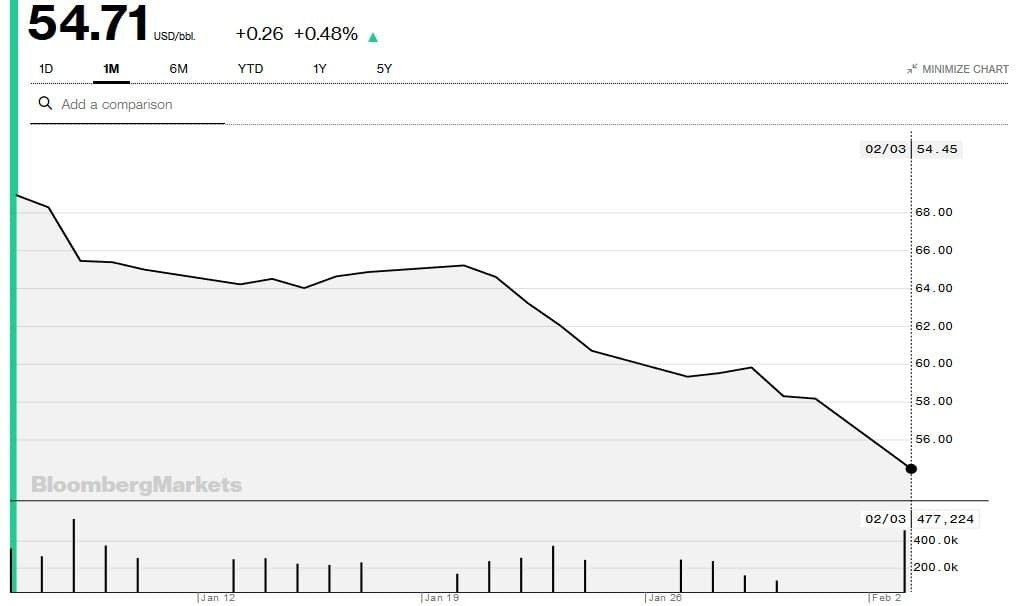

Brent crude prices have dropped 21 percent over the past 30 days, less than two months after the first coronavirus case was reported in the Chinese city of Wuhan. Nearly 60 million people in the country remain under lockdown in the cities as international researchers frantically race to develop a vaccine that will halt the spread of the virus.

Brent Crude Price 1-Month Change

Bear Stampede

According to the Commitments of Traders (COT) report by the CFTC, hedge funds and other money managers sold petroleum futures and options in the six most important contracts equivalent to 147 million barrels in the week ending Jan. 28. Contracts that were out of favor include Brent (27 million), NYMEX and ICE WTI (56 million barrels), US gasoline (28 million), US diesel (16 million) and European gasoil (20 million).

This marked the largest sale by funds in any one week since July 2018 and among the heaviest sales over the past eight years.

That’s quite alarming considering that fund managers have largely remained bullish even in the midst of the ongoing bear stampede. To be fair, fund selling in oil has been going on since January 7; however, it was initially in only small volumes, mostly reflecting profit-taking after a large accumulation of bullish positions over much of last year. But the wave of selling has now accelerated with funds having sold a total of 236 million barrels of crude and products over the last three weeks compared to purchases of 533 million barrels over the previous three months.

Also on rt.com China prepares to roll out more measures to bolster economyFollowing the latest wave of selling, hedge fund positioning in crude and products has fallen to 4:1 with bullish long positions outnumbering bearish short ones. That’s below the long-term average of 5:1 and a sharp turnaround of a 7:1 long-short ratio at the start of the year.

Demand Shocks

Oil traders appear justified in their anticipation for oil consumption to take a massive hit in the short term.

Last week, Bloomberg reported that Chinese oil demand had dropped by about 3 million barrels a day, or ~20 percent of total consumption. The drop marks the largest demand shock in the market since the global financial crisis that ended in 2009. It’s also the most sudden shock the market has suffered since the September 11 attacks nearly two decades ago.

It remains to be seen what measures OPEC and its allies will take to ameliorate the situation when they meet on Tuesday and Wednesday. Helima Croft, global head of commodity strategy at RBC Capital Markets, has told CNBC that the cartel could lower production by another million barrels per day or risk further collapse in prices. It’s going to be a tough call though for the members to agree to such a heavy cut considering that the group had already agreed to deeper production cuts in December.

Selloff Overdone

Investors typically hate uncertainty, and this is the key reason why the coronavirus has been wreaking so much havoc on financial markets. China’s lunar new year has already been extended with many businesses and factories remaining shut with little clarity regarding when the situation will be contained. Meanwhile, several prominent airlines have suspended flights to China while the US, Australia, Japan, Italy, Russia, Pakistan and Singapore have issued a travel ban that prevents travelers that have been to China in recent weeks entry into their respective countries.

While it’s almost inevitable that oil demand will suffer in the short-term, not everybody believes that the sky is falling or that the heavy oil selloff is merited.

Also on rt.com OPEC may deepen production cuts as global oil demand at riskVandana Hari, founder and CEO of energy markets consultancy Vanda Insights, says it’s unfair to compare the coronavirus epidemic to the SARS outbreak of 2003 because the last one was compounded by the US invading Iran. Vandana notes that the fear premium peaked before the invasion, with oil prices falling from $30/barrel to $20/barrel before recovering rapidly after OPEC quickly stepped in and filled the gap left by Iran.

Vandana sees OPEC stepping in to defend Brent at the $60/barrel psychological floor though she says it’s a bit premature for the organization to do so at this time.

S&P Platts is also a bit more bullish about the situation and sees the effects of the coronavirus cooling off around June-July.

This article was originally published on Oilprice.com